If you’ve recently suffered property damage, you’re probably feeling overwhelmed, and now you’re trying to figure out how to handle the insurance claim. It’s stressful enough without a loss adjuster stepping in and using clever tactics to reduce your payout.

But here’s the truth: loss adjusters don’t work for you – they work for the insurance company. And their goal? To save the insurer money.

This guide reveals exactly what loss adjusters do, the most common loss adjuster tricks they use, and – most importantly – how to protect yourself and your claim. If you’re encountering delays, vague answers, or pressure to settle quickly, understanding these tricks could be the difference between a fair payout and a costly mistake.

Who Loss Adjusters Really Work For

Understand their proper role in the claims process – and how their loyalty to the insurer can affect your settlement.

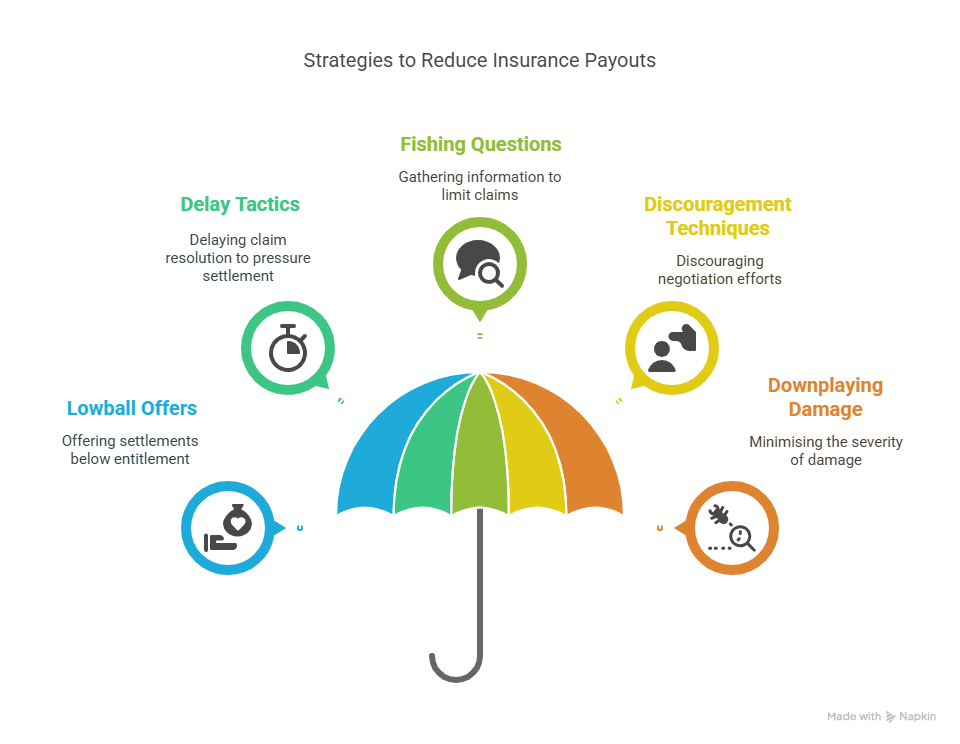

The Tactics They Use to Reduce Your Settlement

Learn the most common strategies used to minimise payouts, including lowball offers, delay tactics, and discouragement techniques.

Red Flags to Watch Out For

Be aware of vague communication, pressure to settle quickly, and reluctance to provide written documentation – clear signs that your claim may be at risk.

How to Protect Yourself

Get actionable tips on documenting everything, managing conversations carefully, and gathering solid evidence to support your claim.

When to Get a Professional on Your Side

Find out when it makes sense to bring in a loss assessor or legal expert who can handle negotiations and protect your interests.

Straight Answers to Common Questions

We answer the key questions every policyholder should ask, such as whether you’re required to give a recorded statement and how to respond to a low offer.

Your Next Steps Checklist

A practical step-by-step plan to help you stay organised, confident, and in control throughout your insurance claim process.

A loss adjuster is sent by your insurance company to assess the damage and determine how much they’ll offer you. While they may appear helpful, they work for the insurer, not for you.

There are two main types of loss adjusters to be aware of:

1. Company-Appointed Adjusters

These adjusters are employed directly by the insurance company. Their priority is to protect the insurer’s interests, and they’ll often aim to reduce claim payments.

2. Independent Adjusters

While not employed by one specific insurer, independent adjusters are contracted by insurance companies on a case-by-case basis. Much like company-appointed adjusters, they ultimately represent the insurer’s interests.

Being aware of who the adjuster works for is essential when preparing to negotiate your claim. They may appear empathetic, but their primary goal will be to save their employer money.

If you’re submitting a claim, it’s important to understand some of the strategies and “tricks” loss adjusters may use to settle for less:

One of the most common tactics is offering settlement amounts far below what you’re entitled to. They’ll often frame this offer as “generous” or “fair,” hoping you’ll accept without pushing back.

Loss adjusters may delay resolving your claim, hoping that the frustration or financial pressure will prompt you to settle quickly and for less.

Adjusters may ask seemingly casual questions early on to gather information that could be used to deny or limit your claim. Even innocent statements you make can be taken out of context.

Some adjusters might downplay the chances of your claim being successful or suggest that further negotiation will be a waste of time.

After examining your property or reviewing documentation, they might insist the damage is less severe than it actually is, leading to a reduced payout.

By understanding these common loss adjuster tricks, you can better protect your interests during the claims process.”

What Oakleafe Clients Say:

Book your complimentary consultation with our insurance claim professionals.

Our insurance claim professionals will explain the claim process to ensure you understand your options.

Recognising loss adjuster tricks early can save you money. Watch out for these red flags:

If you feel like the adjuster’s questions or explanations are vague, it could be a strategy to confuse or mislead you.

An adjuster pushing you to agree to their first offer quickly is likely trying to avoid giving you time to evaluate or dispute it.

If they avoid emailing or providing detailed documentation, it may be an attempt to cloud the claims process.

Long, drawn-out waits for responses are often a stalling strategy.

This isn’t inherently suspicious, but always think carefully before agreeing, as anything you say could be misinterpreted to weaken your claim.

Being prepared with the right strategies can make all the difference when handling a loss adjuster. Here’s how to respond effectively:

Keep a thorough record of all communication with the adjuster, including emails, phone calls, and meeting notes. Consider recording in-person conversations (where legal) and ensure you have physical copies of all evidence and correspondence.

When speaking to the adjuster, keep your responses measured and factual. For example, if they ask for your opinion on damages, respond with, “I’ll need to review that further.”

Insist that the adjuster provides every detail of their assessment and settlement offer in writing. This ensures you can review and dispute any inaccuracies.

Take detailed photographs or videos of the damage before repairs begin. This visual evidence is crucial for verifying the extent of your claim. Supporting documentation, such as invoices and repair quotes, also reinforces your case.

If you feel unsupported or negotiations with the adjuster aren’t progressing favourably, consider hiring a loss assessor (someone who works for you) or seeking legal help.

Sometimes, handling a claim on your own becomes overwhelming or too complicated. Here’s when you might consider getting professional help:

Claims involving significant damage, such as those related to fire or flood incidents, often require expert knowledge to negotiate effectively.

If the back-and-forth discussions with an adjuster aren’t going anywhere, a loss assessor or solicitor can help cut through the red tape.

Repeated delays in your claim being processed are another sign it’s time to bring in an expert.

Loss assessors, for example, are independent professionals who represent you, not the insurer. They handle everything from negotiating with loss adjusters to preparing official documentation, ensuring you receive the maximum payout to which you’re entitled.

Understanding common loss adjuster tricks can help you avoid pitfalls and make informed decisions during your claim. Here are answers to some of the most frequently asked questions.

Can I refuse to meet a loss adjuster?

While you can’t outright refuse to engage with a loss adjuster (this could harm your claim), you are within your rights to reschedule meetings until you feel adequately prepared.

Do I have to agree to a recorded statement?

No, you’re not obliged to provide a recorded statement if you choose to, be mindful of your words and keep responses short and factual.

How quickly should I accept an offer?

Avoid rushing into accepting any offer. Take the time to review it thoroughly and seek a second expert opinion if you’re unsure.

What do I say if they ask what caused the damage?

Stick to the facts. Avoid speculating or guessing the cause of damage; instead, simply state what you observed.

Can I negotiate a low settlement offer?

Absolutely. Request written documentation of how the offer was calculated and present evidence to justify why a higher settlement is warranted.

Getting the best outcome from an insurance claim starts with knowledge and preparation. While loss adjusters may present themselves as neutral, their loyalty lies with the insurer, and their goal is to minimise payouts. Understanding common loss adjuster tricks is your best defence. By recognising their tactics and knowing how to respond, you can avoid costly mistakes and secure a more favourable settlement.

Key Takeaways:

Next Steps:

Remember: the claims process doesn’t have to leave you feeling powerless. With the right knowledge and support, you can take control and ensure the odds are stacked in your favour.

Oakleafe Claims have represented policyholders and managed their insurance claims since before the First World War. We have vast expertise and experience in both domestic and commercial insurance claims with thousands of satisfied policyholders who have received their deserved insurance settlement.

What Oakleafe Clients Say:

Please complete the form and one of our insurance claim professionals will call you back ASAP