Storm damage insurance claims. When a storm barrels through your neighbourhood, it doesn’t just shake trees – it shakes your peace of mind. One minute your roof is intact, the next it’s scattered across the garden. And then comes the sinking feeling: Will my insurance even cover this?

You’re not alone in wondering what your home insurance really protects when extreme weather hits. Storm damage insurance can feel confusing, full of vague terms and exclusions that only seem to show up when it’s too late.

This guide cuts through the jargon and gives you clear, practical answers. We’ll explain what storm damage insurance is, what your home insurance is likely to cover, how to make a strong claim, and how to protect your property before the next storm hits. Whether you’re dealing with broken tiles, waterlogged walls, or fallen trees, we’re here to help you regain control, starting now.

Steps to Make a Claim

Is It Worth Claiming?

Sometimes it’s better to pay for small damage yourself so your insurance price doesn’t go up later.

How to Protect Your Home Next Time

Get Help: You can hire a professional (called a loss assessor) to help you get the most money from your insurance if your home gets damaged.

Storm damage insurance is a type of cover included in most standard home insurance policies in the UK. It’s there to help you recover the costs of damage caused by strong winds, hail, heavy rain, or lightning.

When we talk about storm damage, it typically refers to harm to your home caused by extreme weather events. For example:

Your home insurance policy will usually include “storm cover,” which protects you against such events. But not all policies are created equal, so it’s important to check the specifics of what yours includes.

The short answer is that most home insurance policies do cover storm damage. That said, insurance providers have guidelines to help determine whether damage is classed as being caused by a storm.

How Do Insurers Define a Storm?

There’s no universal definition, but insurers typically look at:

It’s worth knowing that insurance firms often refer to weather reports from services like the Met Office to verify storm conditions in your area.

Policy Exclusions

While storm damage cover is quite standard, there are exclusions you should be aware of:

Review your policy terms carefully to understand your coverage and exclusions.

What Oakleafe Clients Say:

Book your complimentary consultation with our insurance claim professionals.

Our insurance claim professionals will explain the claim process to ensure you understand your options.

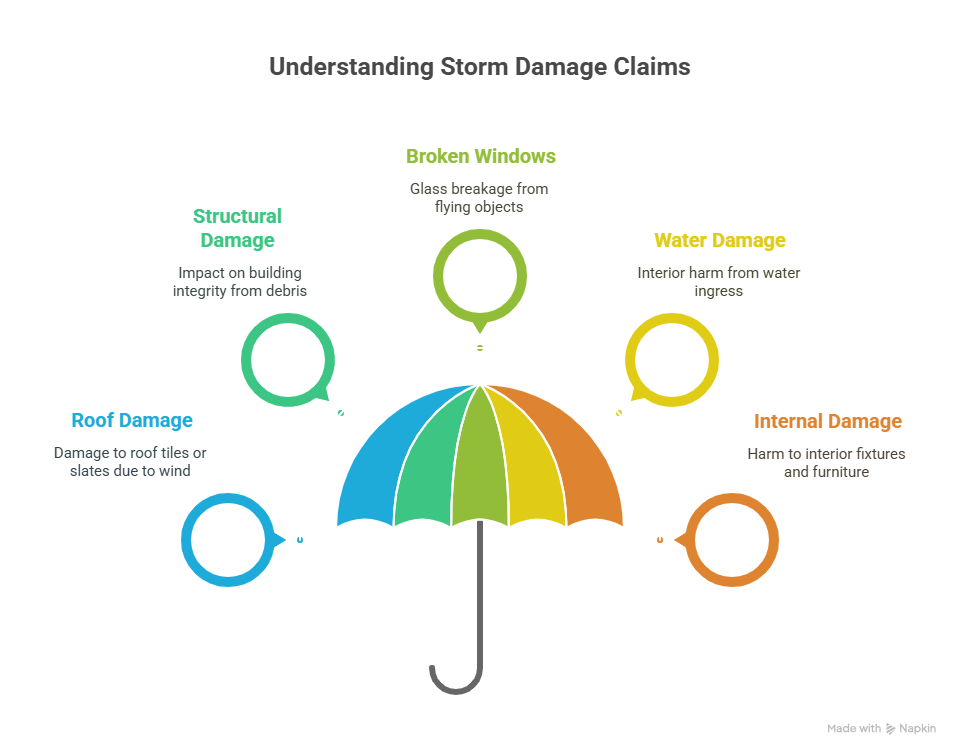

Storm damage affects properties in various ways. Here are some common examples of damage you can claim for:

1. Roof Damage

Strong winds often result in missing slates or tiles. If your roof is partially or fully damaged due to a storm, this is typically covered under storm damage in your home insurance policy.

2. Structural Damage

Fallen trees or debris can impact the structural integrity of your home, such as walls being compromised or garages destroyed.

3. Broken Windows

Flying objects during storms, including hailstones or debris, can result in broken glass.

4. Water Damage

Water ingress through damaged ceilings, walls, or windows can cause significant harm to interiors. Insurers often cover such cases if caused by the storm, not pre-existing issues.

5. Internal Damage

Water damage to insulation materials, electrical fixtures, or furniture is usually covered if directly connected to the storm event.

No matter the extent of the damage, documenting everything with photos and records is crucial (more on that below).

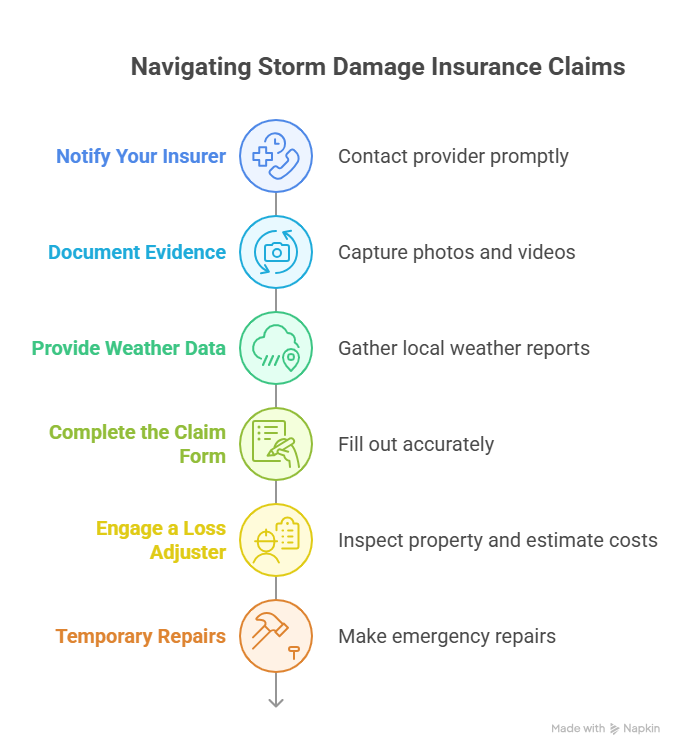

Claiming storm damage can feel overwhelming, but by following a step-by-step approach, you can ensure the process is as smooth as possible.

Step 1. Notify Your Insurer

Contact your provider as soon as possible to notify them about the damage. Most UK insurers have a time frame for reporting claims, so don’t delay.

Step 2. Document Evidence

Take photos and videos of all visible damage. This includes damaged roofs, water stains, broken windows, and any surrounding debris. Strong evidence is key to proving your claim.

Step 3. Provide Weather Data

To support your case, gather local weather reports from the Met Office or other sources showing storm conditions during the event. Your insurer may use this information to validate the claim.

Step 4. Complete the Claim Form

Fill out your insurance claim form accurately and ensure all supporting documents are attached, such as receipts for emergency repairs or contractor quotes.

Step 5. Engage a Loss Adjuster

A loss adjuster may be appointed by your insurance company to inspect the property and estimate repair costs. Consider hiring your own loss assessor to ensure your interests are represented too.

Step 6. Temporary Repairs

Make emergency repairs like boarding up windows or using tarpaulin to prevent further damage—but seek insurer approval beforehand to ensure costs can be reclaimed.

One of the main reasons storm damage insurance claims get denied is the lack of sufficient evidence proving the damage resulted from a storm. Here’s how you can build a strong case:

Investing effort in this early will save hassle down the line.

Before making a claim, evaluate whether it’s worth pursuing. Here are some points to consider:

Preventative measures can help minimise the risk of future storm damage:

Investing in these precautions ensures you’re better prepared for whatever nature throws your way.

Once your claim is submitted, the insurer will process it and decide on a settlement:

To avoid disputes, hiring a loss assessor can make a significant difference in ensuring a fair outcome.

Storm damage can leave more than just physical destruction—it creates stress, confusion, and uncertainty about what to do next. But with the right knowledge and preparation, you can protect both your home and your finances.

Let’s recap the essentials:

👉 Next Steps:

Don’t let the storm win. Get the clarity and support you deserve.

Oakleafe Claims have represented policyholders and managed their insurance claims since before the First World War. We have vast expertise and experience in both domestic and commercial insurance claims with thousands of satisfied policyholders who have received their deserved insurance settlement.

What Oakleafe Clients Say:

Please complete the form and one of our insurance claim professionals will call you back ASAP