Roofing insurance claims for storm damage. When a storm tears through your neighbourhood, it’s not just your roof that takes a beating – your peace of mind often takes a hit too. Many homeowners find themselves staring at damaged shingles or leaking ceilings, unsure of what steps to take or whether their insurer will even cover the costs. If this sounds familiar, you’re not alone – and you don’t have to face it without guidance.

This article lays out everything you need to know about roofing insurance claims for storm damage in the UK. From what your policy actually covers to how to document the damage and make a successful claim, this guide will help you protect both your home and your financial well-being. Whether you’re dealing with missing tiles or serious structural issues, knowing your rights and responsibilities can make all the difference.

What Happens If a Storm Damages Your Roof?

When big storms occur, your roof can become damaged – tiles might fall off, water may leak in, or a tree could crash into it. This can be extremely stressful, especially when you’re unsure if your insurance will cover the repair.

What Your Home Insurance Might Cover:

It usually helps pay for damage from storms, like:

But it won’t help if:

What You Should Do After a Storm:

How to Make a Claim (Ask Insurance to Pay):

How to Be Ready Before a Storm:

Common Problems to Watch Out For:

Easy Tips to Remember:

Understanding whether your home insurance covers storm damage is crucial before filing a claim. Insurance providers typically define a “storm” based on specific thresholds, such as wind speeds exceeding 55 mph or hailstones larger than a certain size.

What does a standard policy cover?

Most home insurance policies include coverage for:

What is usually excluded?

However, policies often exclude:

To clarify your coverage, carefully review your policy document or contact your insurer.

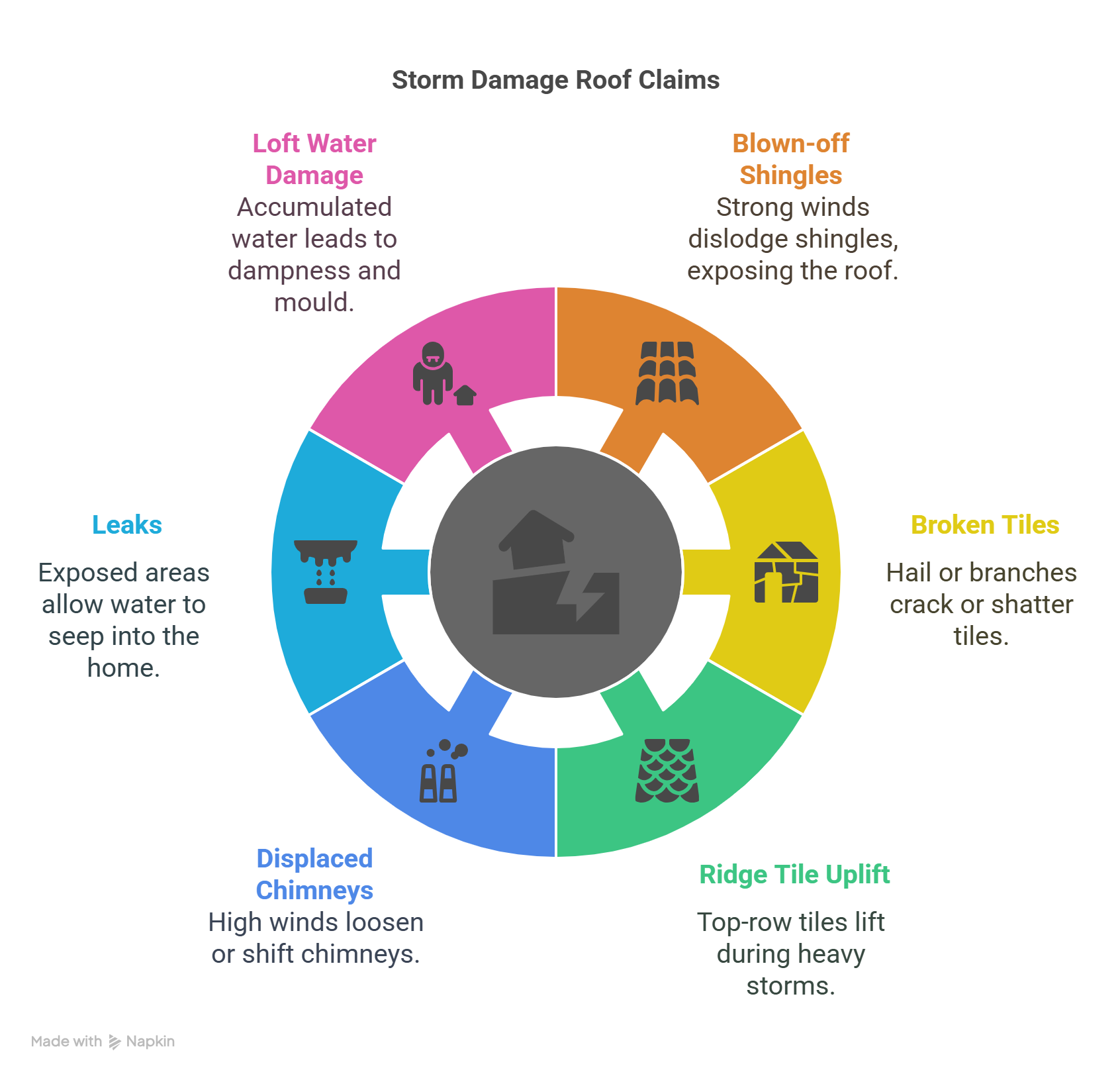

Different types of storm damage may affect your roof depending on the roofing material and the severity of the storm. Here are some common examples:

1. Shingles and Tiles

2. Structural Shifts

3. Water Damage

What Oakleafe Clients Say:

Book your complimentary consultation with our insurance claim professionals.

Our insurance claim professionals will explain the claim process to ensure you understand your options.

Insurers require clear evidence of storm damage to approve your claim. Here’s how you can make your case stronger:

1. Gather Photographic Evidence

Take clear, high-quality photos of the damage from multiple angles. Ensure these are date-stamped or stored in a device with automatic metadata.

2. Obtain a Roofing Surveyor’s Report

A professional report can identify the type and extent of the damage, providing an objective assessment recognised by insurers.

3. Collect Weather Reports

Request weather data for the date and location of the storm. Insurers often verify claims against recorded conditions, such as wind speeds and rainfall levels.

4. Track Pre-Storm Maintenance

Maintaining a log that documents regular roof inspections and repairs can help counter claims of negligence by your insurer.

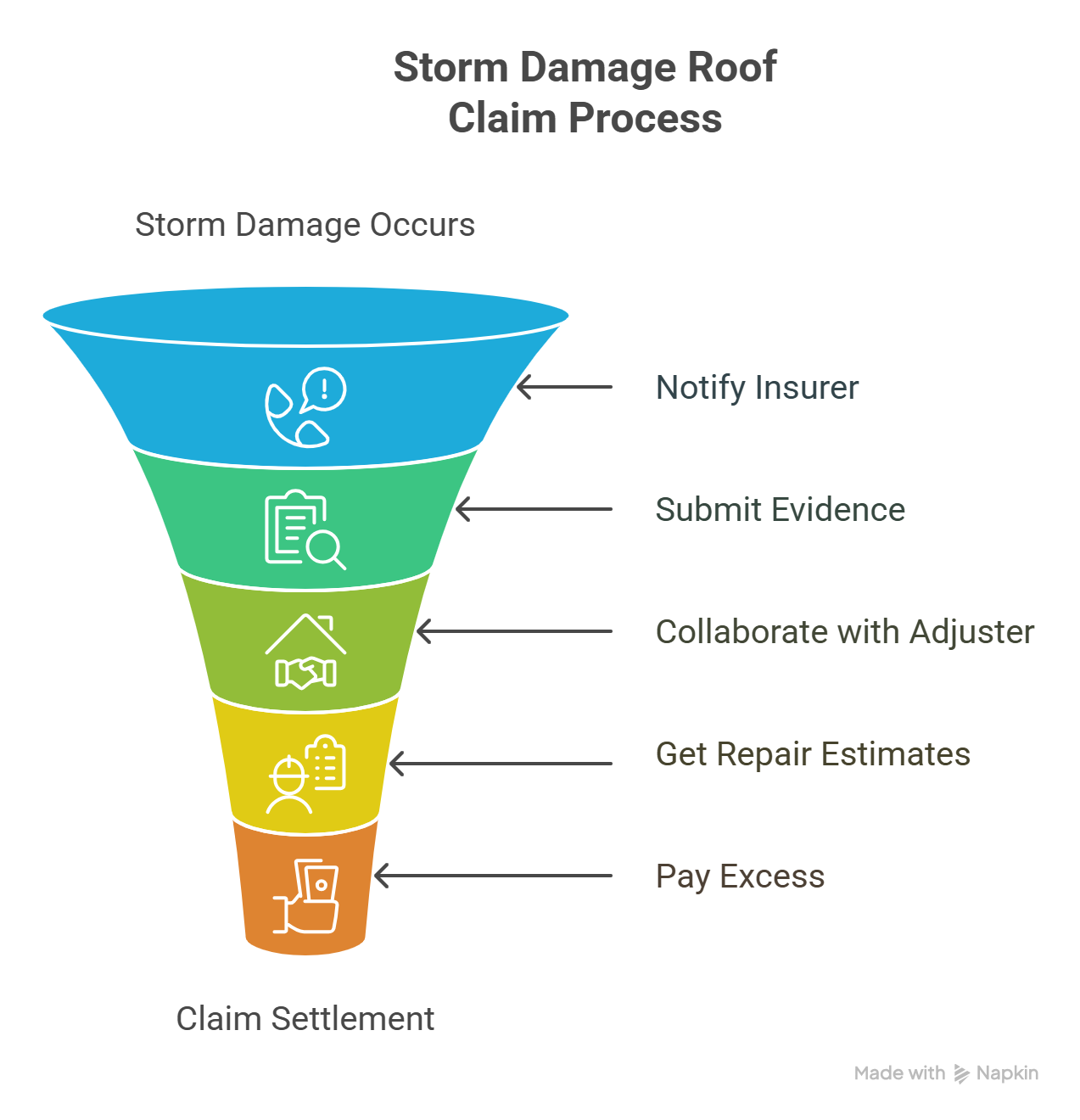

Making a claim can be a daunting process, but breaking it into manageable steps can make it a lot easier:

Step 1: Act Immediately

Notify your insurer as soon as possible. Most policies have a claim window, and delays can lead to rejection.

Step 2: Submit Evidence

Provide all documentation, including:

Step 3: Collaborate with the Loss Adjuster

The insurer will assign a loss adjuster to evaluate the claim. Be cooperative but mindful that their role is to protect the insurer’s interests.

Step 4: Get Repair Estimates

Obtain quotes from reputable roofing contractors. This will help verify the cost of repairs and avoid underestimation by the adjuster.

Step 5: Pay the Excess

Most policies require the policyholder to pay an excess before the insurer covers the rest. Ensure you’re clear on this amount beforehand.

These steps form the foundation of successful roofing insurance claims for storm damage, especially when time and accuracy are critical.

Taking proactive steps can protect your roof from storm damage while also strengthening any future claims:

Even with the best preparation, challenges can arise when filing a claim. Some common pitfalls include:

1. Wear-and-Tear Exclusions

Insurers often reject claims by citing pre-existing damage or general wear and tear.

2. Ambiguous Policy Wording

Terms like “storm” can be defined differently by insurers, causing disagreements.

3. Late Reporting

Failing to notify your insurer promptly may result in denied claims.

To avoid these issues, ensure you understand your policy and take action promptly after a storm.

Here are quick answers to common questions about roofing storm damage claims:

Delays in reporting, lack of evidence, and policy exclusions are frequent problems. Insurers may also dispute what qualifies as “storm damage.”

Yes, your premium may rise after a claim, but this depends on your insurer and the policy terms.

Most policies cover damages caused by fallen trees, but not the cost of removing the tree itself.

You can challenge the decision by seeking advice from a loss assessor or filing a complaint with the Financial Ombudsman.

Storm damage to your roof can be devastating, but understanding your insurance policy and knowing how to approach the claims process puts you back in control. With clear documentation, prompt action, and the right support, you can significantly improve the chances of a successful claim.

Key Takeaways:

What to Do Next:

Need help with a storm-related roof claim? Don’t go it alone. Contact Oakleafe Claims today and let experts handle the stress while you focus on recovery.

Oakleafe Claims have represented policyholders and managed their insurance claims since before the First World War. We have vast expertise and experience in both domestic and commercial insurance claims with thousands of satisfied policyholders who have received their deserved insurance settlement. With no upfront fees required, our internal data shows that insurance claims managed by professional loss assessors like Oakleafe can expect a settlement up to 40% higher than claims managed by the policyholder.

What Oakleafe Clients Say:

Please complete the form and one of our insurance claim professionals will call you back ASAP