How to claim insurance after a theft is one of the most common questions UK residents ask following a burglary. And it’s no surprise – getting it wrong can lead to delays, disputes, or even a reduced payout.

A break-in is more than just the loss of valuables. It’s a personal violation that leaves many feeling shaken and vulnerable. On top of the emotional impact, you’re faced with the daunting task of navigating an insurance process that can feel slow, unclear, and overwhelming.

But you don’t have to face it alone—or guess your way through it. Whether you’re dealing with stolen jewellery, a damaged door, or both, this guide will walk you through each critical step: from reporting the theft and gathering evidence to working with your insurer and securing the right support.

By the end, you’ll know exactly how to claim insurance after a theft, confidently, and without missing any key steps.

1. What to Do Immediately After a Theft

2. Documenting Stolen Items and Proving Ownership

3. Contacting Your Insurance Provider

4. Understanding Your Insurance Policy

5. How a Loss Assessor Can Help You

6. Working Through the Insurance Claim Process

7. Preventing Future Theft

8. Quick Recap and Key Takeaways

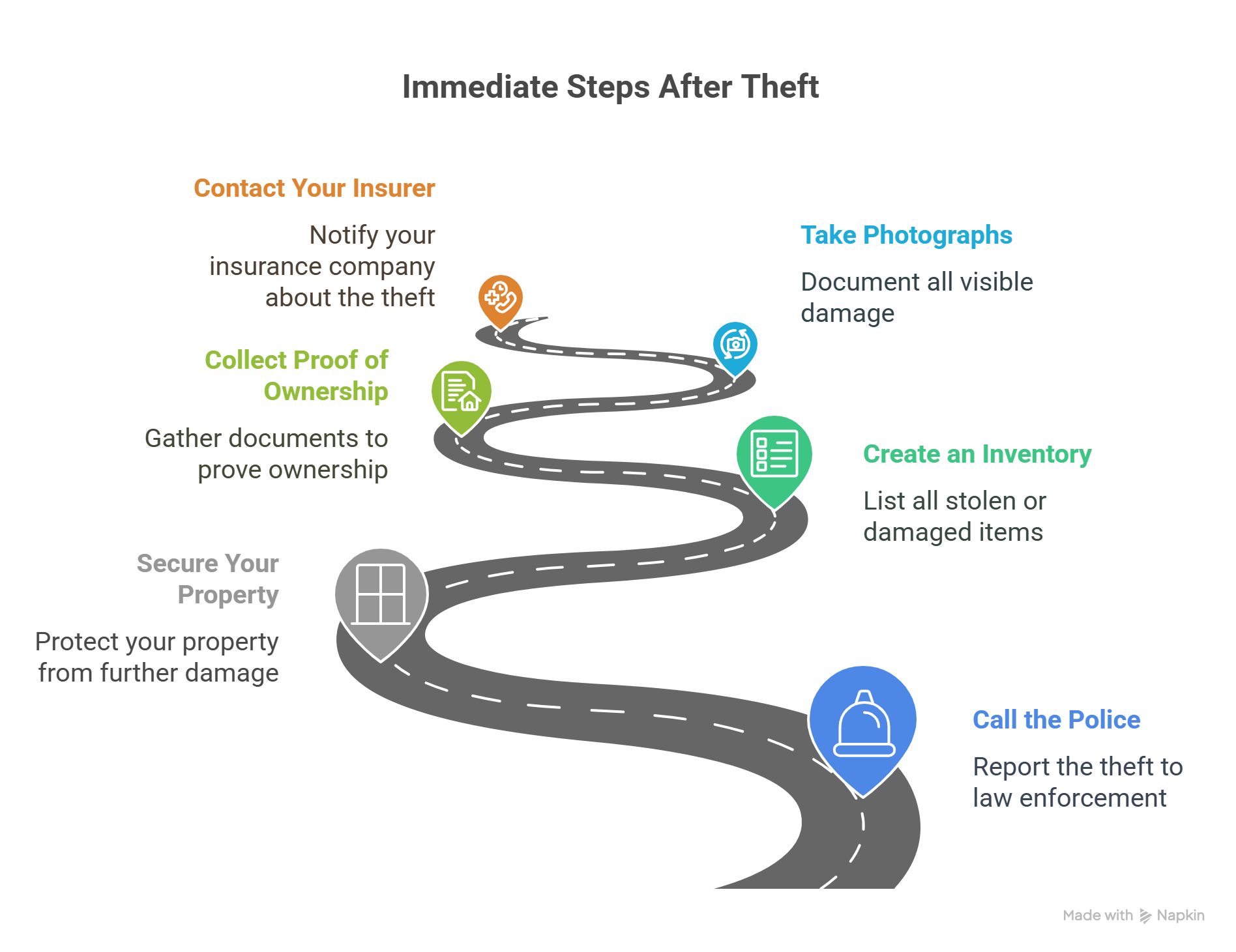

The first few hours after a theft are critical. Acting fast can help police investigations and safeguard your insurance claim.

1. Call the Police

2. Secure Your Property

If there has been forced entry or damage:

Good documentation is your strongest ally in a successful claim.

Create an Inventory

Collect Proof of Ownership

Take Photographs

What Oakleafe Clients Say:

Book your complimentary consultation with our insurance claim professionals.

Our insurance claim professionals will explain the claim process to ensure you understand your options.

Once you’ve reported the theft and documented your losses, it’s time to notify your insurer.

Notify Within the Policy Timeframe

Most insurance policies have clear deadlines for reporting incidents. Review your policy and ensure you file your claim within the specified timeframe to avoid rejection.

Choose a Contact Method

Insurers typically allow claims to be filed via:

Having your policy number, crime reference number, and documentation ready will simplify the process.

Role of a Loss Assessor

If your claim appears complex, you might benefit from hiring a loss assessor. They:

While assessors take a fee (often a percentage of the claim settlement), their expertise can drastically increase the likelihood of a successful claim.

Knowing your policy details is key when learning how to claim insurance after a theft, especially when it comes to what’s covered and what’s not.

Types of Cover

Common Exclusions

Be aware of typical exclusions that may affect your claim:

Refer to your policy schedule to identify other potential exclusions.

The claim process involves submitting your documentation and working with your insurer to achieve a settlement. Here’s what to expect.

Submit Documentation

Provide all the necessary paperwork, including:

Adjuster or Loss Assessor Visit

Your insurer’s loss adjuster may visit your property to:

If you’ve hired a loss assessor, they will liaise with the adjuster on your behalf.

Settlement or Rejection

Once all details are reviewed, the insurer will:

If your claim is rejected, request specific reasons and, if necessary, appeal the decision with additional supporting evidence.

Experiencing theft can be distressing, but implementing security measures can reduce the likelihood of future incidents.

Improve Your Home Security

Consider upgrading your home’s security setup:

Join a Neighbourhood Watch Scheme

Collaborating with local residents in a community-based initiative can:

Check Your Insurance Coverage

Now is a good time to revisit your policy terms:

Recovering from a theft is never easy, but with the right approach, you can take back control and increase your chances of a successful insurance claim. Acting fast, staying organised, and understanding your insurance cover makes a big difference.

Here’s a quick recap of what you should do:

If you’re feeling overwhelmed or unsure what your insurer might cover, Oakleafe Claims can help. Our expert loss assessors handle the heavy lifting, fight your corner, and ensure your claim is maximised. Don’t leave your payout to chance – speak to a professional today and get the support you deserve.

Oakleafe Claims have represented policyholders and managed their insurance claims since before the First World War. We have vast expertise and experience in both domestic and commercial insurance claims with thousands of satisfied policyholders who have received their deserved insurance settlement.

What Oakleafe Clients Say:

Our claims team will review the details and contact you shortly. We’ll guide you through the next steps of your claim.